Reflections on a changing US healthcare market: what’s the impact on digital health innovators?

Posted on

Following a trip to the US in January for the StartUp Health Festival and Health 2.0 WinterTech, DigitalHealth.London Programme Director Yinka Makinde shares the key highlights of these high-profile events, and reflects on how the new US administration could impact the digital health market in the US and UK.

January saw four key digital health events hosted in the US: CES 2017, JP Morgan Healthcare Conference, StartUp Health Festival, and Health 2.0 WinterTech.

CES, a consumer device show, is focussed entirely on the latest shiny ‘toys’ set to disrupt the healthcare market. JP Morgan Healthcare Conference is more investor focussed, evaluating the latest trends, solutions and services on the market.

StartUp Health Festival is different, with a focus on two things:

- articulating the problems that exist within healthcare, globally as ‘Moonshots’

- building an army of global Health Transformers (aka innovators), who are on a mission to solve these big problems.

The US is recognised for driving the digital health market over the last five years, in part due to the regulatory, legal and technological trends originating there that have helped to accelerate the uptake of digital innovations throughout the world. This has created a global perception that the US market is more open to innovation and a place where the opportunities to build and sustain digital-focused companies are the most prevalent and fruitful.

The US has traditionally been dominant in its funding levels in the digital health market. But in 2015 and 2016, there were signs that global digital health investment (and innovation activity) is increasing. StartUp Health, which monitors global investment activity (and deals less than $2 million), reported a record year for digital health investment in 2016, at a total of $7.9 billion, with a rise in the number of significant non-US investments in digital health.

The top 3 largest deals closed in 2016 were:

- Onduo (France/ US) – a Sanofi & Verily Life Sciences joint venture, with a Diabetes focus.

- Ping An Good Doctor (China) – an app providing free diagnosis, treatment and online appointment booking, enabling users to consult doctors through text, pictures, and video.

- Babytree (China) – Providing online parenting diaries, parenting knowledge, early-education kits/products.

Highlights from StartUp Health

StartUp Health Festival was a two-day event in San Francisco attracting 2,500 guests, with an awesome line-up of speakers and keynote guests. Some key takeaways for me were:

Toby Cosgrove, MD, CEO & President, Cleveland Clinic, who spoke about how Cleveland Clinic is winning the fight to reduce the high costs of health service delivery through the introduction of virtual visits and group consultations.

Steven J Corwin, MD, CEO NY-Presbyterian Hospital, spoke about their use of kiosk visits in emergency rooms to reduce waiting times from two hours to 30 minutes. He also reflected a reality that currently EMRs are making clinicians less productive, hence the need to explore Artificial Intelligence and Machine Learning to address this.

Mental health, vulnerable patients, standards of care, and reducing variation were all themes that seemed to be universally articulated across the panels.

Unity Stokes and Steve Krein, co-founders of StartUp Health unveiled their 25 year vision to organise and support a global army of health transformers to achieve 10 Health Moonshots to improve the health and wellbeing of every person in the world. From 4,500 applications from innovators since 2011, they have selected 180 high potential companies so far to support as part of their vision.

StartUp Health announced new partnerships with SAP and Allianz, in helping to achieve the objectives of its Moonshots. These include the Cancer Moonshot, Access to Care Moonshot and Mental Health & Wellbeing Moonshot. Bill McDermott, seduced the audience with an engaging story of his journey from a being Deli owner to now CEO of SAP.

Jonathan Bush (nephew to George W. Bush), CEO & Co-founder AthenaHealth (a partner of StartUp Health), provided an energetic and entertaining perspective on the uncertain political landscape and its impact on selling into the healthcare sector in the US; balancing convenience against price; and the growing importance of risk contracts for providers to ensure some leverage for innovation adoption.

For entrepreneurs, Vinod Khosla, Partner at Khosla Ventures, offered the advice: “figure out how to stay alive for long enough, in order for lady luck to make an impact” [context: luck plays a big role in the success of a start-up].

Promoting the value of Artificial Intelligence, he reflected on the fact that a human being cannot possibly keep up with all the latest research and clinical information required to reduce diagnostic errors. So let machines do what they do well, and remove doctors from this specific process.

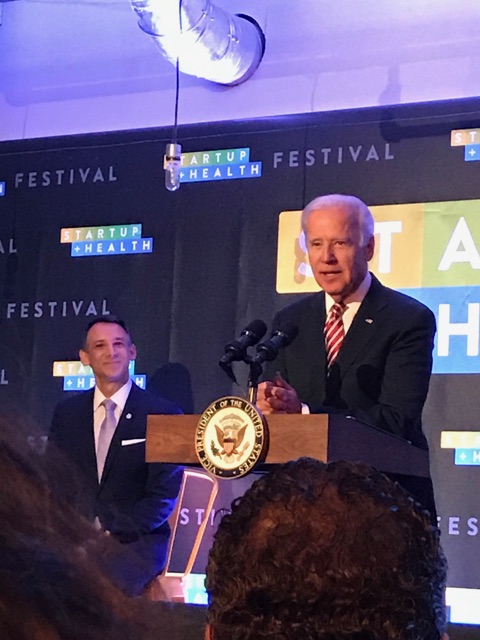

Finally, the icing on the cake for me was hearing the emotional speech from ex Vice President Joe Biden about the Cancer Moonshot, which he leads. Committed to championing the fight against cancer for the rest of his life, and appealing to the global audience that he needs our help, as we must change the system in order to fight cancer.

Finally, the icing on the cake for me was hearing the emotional speech from ex Vice President Joe Biden about the Cancer Moonshot, which he leads. Committed to championing the fight against cancer for the rest of his life, and appealing to the global audience that he needs our help, as we must change the system in order to fight cancer.

I thoroughly enjoyed representing DigitalHealth.London, the London market, being interviewed, meeting in person Dr Jordan Shlain, MD one of the keynote speakers invited for the upcoming DigitalHealth.London/collaborate event, and meeting a number of interesting SMEs – some of which have some interest in accessing the UK market, which gave me the opportunity to sell the benefits of the DigitalHealth.London Accelerator programme.

Optimism, despite the upcoming health policy changes, was my lasting impression of this festival.

Reflections of a changing US healthcare market: what’s the impact for digital health innovators?

Health 2.0 WinterTech, another conference I attended whilst in the US, in contrast assumed an air which was slightly more foreboding, as the various panels reflected and speculated on the potential impact of ‘Trumpcare’ under the new US administration.

This inspired me to find out more about Obamacare, to gain a better understanding of what these changes could mean to digital health innovators in the US, and the impact on UK companies considering the US market.

US Health Care System

It has been stated that: “health care costs are the number one cause of bankruptcy in the US”. A single visit to the emergency room costs $1,265 on average. A broken foot costs around $16,000 while cancer treatment can cost $30,000.

Many people get health insurance as a benefit from their employer. The employer will usually split the monthly premium cost. Families with health insurance only pay a small fee per visit, called a co-payment.

For individuals and families whose jobs or job status doesn’t provide health insurance (e.g. the unemployed), the options are as follows.

Those poor enough to meet the criteria to qualify for a hardship exemption, can access Medicaid, paid for by state and the Federal governments.

The over 65s go on Medicare and they pay premiums that the Federal government subsidises.

People who make too much money to qualify for Medicaid, are too young for Medicare, but are self-employed or don’t get insurance from their employers, have to pay for their own insurance, which is usually very expensive.

Before Obamacare, many people took the risk and went without health insurance. Those with a chronic illness – called a pre-existing condition – were denied coverage by the health insurers. There were between 32-50 million people who didn’t have health insurance.

For the un-insured, if they needed medical attention and they had to go to the hospital, they often just didn’t pay the bill. The bill, left with the hospital, would be charged to an emergency Medicaid plan, which raised the cost of healthcare for the broader population.

Affordable Care Act – aka “Obamacare”

Amongst other reasons, Obamacare was brought in to:

- Enable families without health insurance to access it by participating in open enrolment on the health care exchanges from 1 November 2016 to 31 January 2017.

- Require everyone to enrol in health insurance by 31 January 2017. Those that didn’t, faced a 2.5 per cent tax on their 2016 Adjusted Gross Income. The minimum is $625 per adult.

- Prohibit insurance companies from denying coverage to anyone with a pre-existing condition.

- Allow more people to access Medicaid.

- Enable most families that earn too much to qualify for Medicaid, to still get help. They can get subsidies every month or even reduced co-payments and deductibles.

The biggest benefit put forward for Obamacare is that it lowers overall healthcare costs, by providing insurance for millions and making preventive care free. People receive treatment before they get to the point of needing expensive emergency room services. It requires all insurance plans to cover ten essential health benefits, including treatment for mental health, addiction and chronic diseases. Such patients risk ending up in the emergency room if they don’t have access to healthcare.

The major negative impacts of Obamacare cited are:

- Many of the 30.1 million people who currently buy private health insurance have had their plans cancelled by their insurance company because the plan didn’t meet the ten essential health benefits. The costs of replacement insurance plans are higher because they provide services, like maternity care, that many people seeking coverage do not actually require.

- Another 3-5 million people could lose their employer-sponsored health care plans.

- Increased coverage may raise overall health care costs in the short-term. That’s because many people will receive preventive care and testing. These additional tests, such as cancer screening and cholesterol tests, will lead to higher medical spending overall.

What do the political changes mean for digital health innovators and companies?

‘Trumpcare’ – a new era

With ‘Trumpcare’ it’s possible that an estimated 21 million people currently receiving federal assistance via Obamacare’s Advanced Premium Tax Credit, cost-sharing reductions, or Medicaid expansion could lose their health coverage if Trump’s healthcare plan becomes law.

There could be a considerably larger onus on costs being passed on to consumers who receive their health insurance through their employer. Americans risk losing their health insurance, in which case hospitals could be on the line for covering the medical care of un-insured people should they need it. Insurers could respond by charging employers more to counteract the higher expenses they face from hospitals. Forcing employers to pass on these expenses to their employees via higher deductible plans that require the employees to pay more out of pocket.

Ultimately, ‘Trumpcare’ could drive a significant increase in the number of people un-insured.

The inevitability is that healthcare spending will continue to increase, which will impact directly on the citizens’ pocket. Republicans are not in favour of healthcare spending growth. For Medicare coverage, the question is around what will be the fixed level of premium contribution that will be offered by the state, and on what basis will this grow incrementally over time?

Therefore what is the delta that will have to be paid for by the US citizen, and who will be able to afford it? Premiums are likely to increase and citizens will be forced to drop out of health insurance plans.

With this bleak future scenario, citizens will be seeking help with smarter shopping for affordable healthcare services and hospitals could be forced to cover the medical care of un-insured citizens should they need it.

So what’s the lesson for innovators? You must choose meaningful problems to solve!

1. Serving the un-insured

Entrepreneurs are still trying to figure out how by targeting low income people, they will get paid by serving this population, and government health programmes like Medicaid and Medicare are struggling to figure out how they’re going to pay providers for approaches that don’t involve a traditional visit to the physician.

Nonetheless, there is growing interest from the investor community in digital health initiatives that target low-income patients, largely due to the sheer numbers, and the scale opportunity this creates.

A few companies are starting to develop propositions for this target market. Text4Baby is a free text-messaging service for pregnant women and new mums, and offers English and Spanish language information about prenatal care, labour and delivery, breastfeeding, developmental milestones, and immunisations, all timed to the baby’s due date.

Since 2010, Text4Baby has reached nearly one million women, more than half of whom in one survey reported annual incomes of less than $16,000.

Omada Health is testing a modified version of its ‘Prevent’ programme; a diabetes and heart disease prevention program targeted at people on Medicaid or who are un-insured. The free program offers patients a digital scale, behaviour coaching and education, access to a personal health coach, and an online peer network. The digital scale doesn’t require a wireless connection, and the patient just needs to be able to access the internet for one hour each week.

2. Serving the Providers

Hospitals will be hit significantly by the anticipated changes in healthcare policy. They way that they will be paid will change, impacting their revenue flow. Further, Obamacare’s subsidised private individual coverage and expanded Medicaid benefits have turned patients who couldn’t afford care previously, into paying customers, allowing hospitals to hire more staff to treat millions of newly insured Americans.

A hospital is often the largest employer in a community, and healthcare facilities have been an economic engine that have helped to reduce unemployment under the Obama administration.

A repeal of the Affordable Care Act could cost more than 2.5 million jobs, many of which would come from the nation’s hospitals and health systems.

One of the opportunities therefore, is for digital health companies that can design services to help make healthcare cheaper by facilitating and enabling care delivery to be shifted from high cost environments to lower cost environments. For instance, shifting care:

- From Inpatient hospitals to Outpatient hospitals

- From Outpatient hospitals to Ambulatory Care Centres

- From Ambulatory Care centres to Physicians clinics

- From Physician clinics to the patient’s home

3. Reassess assumptions about who will pay

For any digital health company looking to sell into the US healthcare market, the question is, who will pay? There are five potential buyers:

- Insurance companies and/or Employer

- Providers (e.g. Hospitals)

- Pharmaceutical companies

- Accountable Care Organisations

- Citizens

Hospitals won’t have a lot of spare cash moving forward. Citizens will be reluctant to have to pay for this stuff. Value based pricing models will continue to grow in importance. Employers may take a more active role on being the buyers of digital health to support their workforces.

4. See ‘evidence’ generation as a necessary competitive requirement

Digital health companies will be pressured to think about how they can demonstrate with a compelling argument, the value of their innovation in terms of patient outcomes, its cost implications to the system, and to the entity it is hoped will pay for the solution.

Companies focussing on the solutions that have the evidence base to show that they reduce the cost of healthcare delivery for the Provider, will shine above the rest. Companies serious about this market will need to factor in FDA approval as a must have, rather than a nice to have if to be taken seriously.

Buying decisions will be increasingly based on science and economics – tangible health outcomes and cost reductions, rather than patient engagement, and consumer populism.

Closing thoughts

My question is, what will be the reverberations of ‘Trumpcare’ on the global digital health market? Will we start to see an increase in digital health imports from the US to Europe, and most notably the UK over the next four years? Will the US still continue to be a ‘plan A’ or ‘plan B’ for UK born digital health startups, disillusioned with the complexities of the NHS and struggling to gain traction? Is UK positioning on the digital health global stage set to be bolstered in the wake of the new US administration?

It’s too early to tell, but I will observe with avid interest, how this landscape evolves.

References:

http://www.forbes.com/sites/brucejapsen/2017/01/08/as-obamacare-repeal-looms-hospitals-brace-for-job-losses/#47b9ec0a29b6

StartUp Health Insights Funding Report 2016 Year End

http://digitalhealthspace.blogspot.co.uk/2017/01/ces-2017-jp-morgan-healthcare-conference.html

https://www.hhs.gov/healthcare/about-the-law/

https://www.thebalance.com/obamacare-pros-and-cons-3306059

https://rockhealth.com/from-obamacare-to-trumpcare-questions-for-digital-health/

http://europe.newsweek.com/trumpcare-cripple-healthcare-system-527630?rm=eu

http://www.standard.net/Government/2016/06/29/Digital-Health-Not-Just-For-Well-Heeled-Fitness-Fiends

Related content

Lessons on outcomes-driven weight management models from eMed fund raising

eMed’s recent raise reveals how AI‑led, outcome‑driven weight management models could shape the future of population health.

Innovator Spotlight: PocDoc

This Innovator Spotlight explores how PocDoc’s landmark funding round is positioning their flagship product as the go-to diagnostic tool for cardiovascular disease.

Dignio acquisition signals remote care international expansion

Summa Equity acquires Norwegian health tech Dignio, backing remote care, telehealth and home monitoring to support scalable healthcare systems amid rising costs, ageing populations and pressures.